Marketed as a Home. Should Have Been Marketed as an Opportunity - Team Ford Realtors Success!

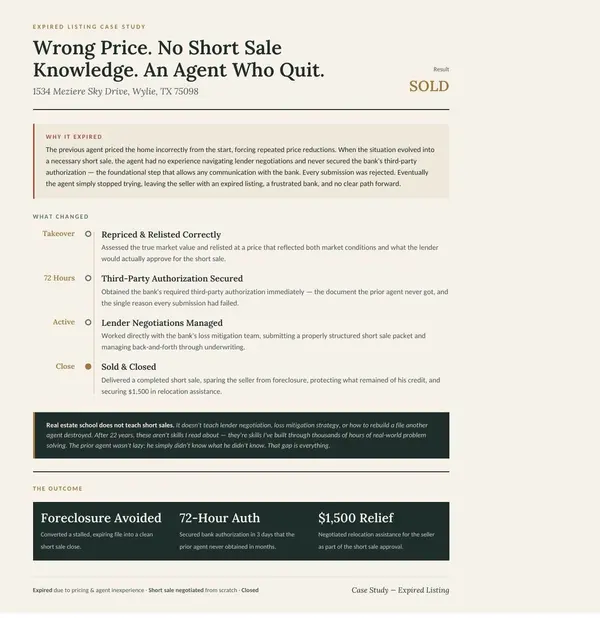

Wrong Price. No Short Sale Knowledge. An Agent Who Quit.

North Texas Housing Market: The Turnaround Has Begun

For the last couple of years, the North Texas housing market has been defined by one word: uncertainty. Rising interest rates, slower buyer activity, and constant “crash” headlines have made many homeowners and buyers sit on the sidelines. But here’s the truth: we are now standing at the turning poi

Categories

- All Blogs (27)

- 75002 Home Statistics (1)

- 75013 Market Overview (1)

- Buying A Home (5)

- Collin County Homes (1)

- Dallas job growth (1)

- Expired Listings (4)

- Grayson County (1)

- Hiring a real estate agent (3)

- Home Sales (4)

- Mortgage (2)

- Plano (1)

- Real Estate News (3)

- Short Term Rentals (1)

- Top real estate agents near me Allen (1)

- Top real estate agents near me Parker (1)

- Top real estate agents near me Plano (1)

Recent Posts

Team Ford Realtors Success: The Price Was Never the Problem. The Marketing Was

Team Ford Realtors Success: The Market Moved. We Moved With It

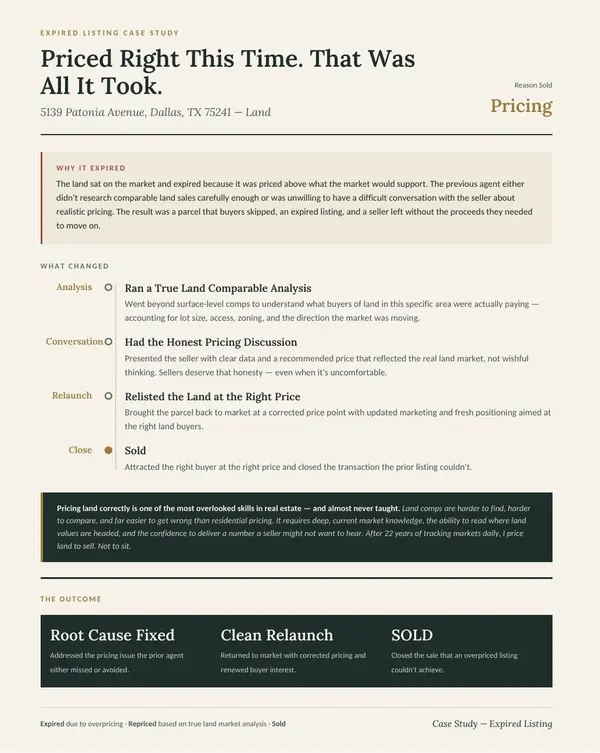

Team Ford Realtors Success: Priced Right This Time. That Was All it Took

Marketed as a Home. Should Have Been Marketed as an Opportunity - Team Ford Realtors Success!

Wrong Price. No Short Sale Knowledge. An Agent Who Quit.

North Texas Housing Market: The Turnaround Has Begun

Mortgage rates drop for third consecutive week

Home Prices Are Dropping in Over a Third of U.S. Markets

Builders Boost Incentives Amid Slower Spring Sales

Buying Land in Texas May Get Tougher—Here’s Why That Matters